Prompt delivery slots disappear

Prompt newbuild delivery slots are becoming rarer than on the record comments from Gianluigi Aponte, the founder of Mediterranean Shipping Co (MSC), the company with more tonnage on order than anyone else.

Latest data from brokers BRS shows owners have next to no chance of getting a ship delivered next year, barring concluding resale deals, while global yards are 87.3% full for 2025 and 80% covered for 2026, enjoying their longest backlogs since 2010.

Yards are reopening to handle the bumper orders with Greek broker Intermodal suggesting 1.5m cgt of extra shipbuilding capacity is being added this year, principally out of China.

Intermodal also predicts utilisation of what it terms as the 80 first-tier yards in the world will increase from 65% in 2022 to 83% in 2023 and further to 91% in 2024.

“[Shipbuilding] prices are expected to remain on the upper limit amidst elevated steel plate prices, labor shortages, inflationary pressures, and restrained shipbuilding capacity,” it said in its latest weekly report.

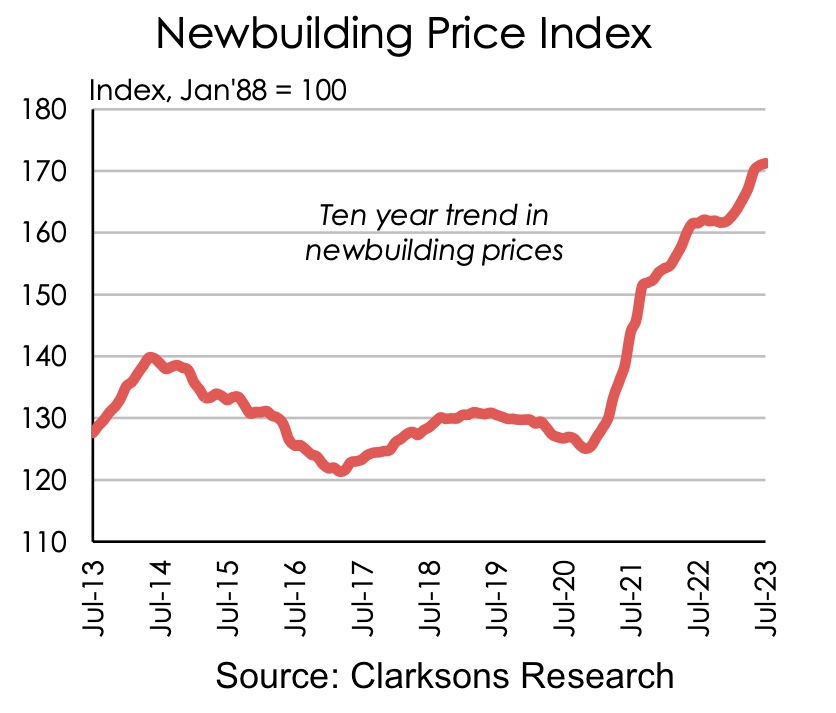

The latest data from Clarksons Research shows a total of 710 vessels have now been ordered in the year to date, down 17% year-on-year on an annualised basis

Tim Smith, a director at Maritime Strategies International (MSI), writing for Splash earlier this month, noted: “The constraint on deliveries remains in place despite the reported reactivation of a large amount of newbuilding capacity over the last year or so. The reality is that much of this resurrection is in the planning or scaling up phase and won’t be contributing meaningfully to output for some time to come.”

This contrasts with ongoing reports of labour shortages at Korean yards and a clear cap on capacity in Japan.

The net effect of this, according to Smith, will be to prolong both the delivery of the current bloated orderbooks for LNG and containerships, which in the process will keep newbuilding prices higher for longer as available berths are pushed into the future.

Clarksons Research data shows newbuild prices have already leaped by more than 6% this year to highs not seen since the last great shipping bull-run which came to a close with the 2008 global financial crisis.

While 2023 has seen far more dry bulk and tanker orders than at any other time in the 2020s, the fact remains that the delivery schedule for these two sectors remains at generational lows, while the global merchant fleet is aging considerably.

The average age of the main fleets is increasing with bulkers now at 11.1 years versus 8.7 years five years ago, tankers standing at 11.7 years versus 10.1 five years ago, and containerships at 13.7 years versus 11.4 in 2018, according to Clarksons data from late February. Clarksons estimates that 31% of the current fleet by tonnage would be D or E rated under the recently enacted Carbon Intensity Indicator (CII) assuming recent trading patterns and no changes in speed or the technology status of vessels.

The impetus to refresh the global fleet has been given greater urgency following last week’s 80th gathering of the Marine Environment Protection Committee (MEPC) at the International Maritime Organization (IMO) where member states agreed on new green targets for international shipping, which according to Dr Christiaan De Beukelaer, senior lecturer in culture and climate at the University of Melbourne and Dr Tristan Smith from UCL Energy Institute will require cuts in emissions per ship of up to 60% by 2030 and as much as 91% by 2040.

splash247